Worked examples

Backtesting & robustness, on a real strategy.

Each example optimizes the founder's own private strategy with TradingTune and compares it against buy-and-hold on historical data over the same period. Open any backtest to see the TradingView chart, the full metric table, and the equity, benchmarking, returns, and trade-analysis screenshots. These are illustrative of the software, not a recommendation.

Warning

About these figures

The figures shown are the founder's own private strategy (the "Smart Momentum Grid"), shown only to illustrate what the software does. They are historical and hypothetical, not for sale, not a recommendation, and not representative of typical or expected results. TradingTune is a backtesting and optimization tool, not financial advice. Nothing here is a recommendation, solicitation, or offer to buy, sell, or hold any security, or to adopt any trading strategy. Trading carries risk of loss.

-

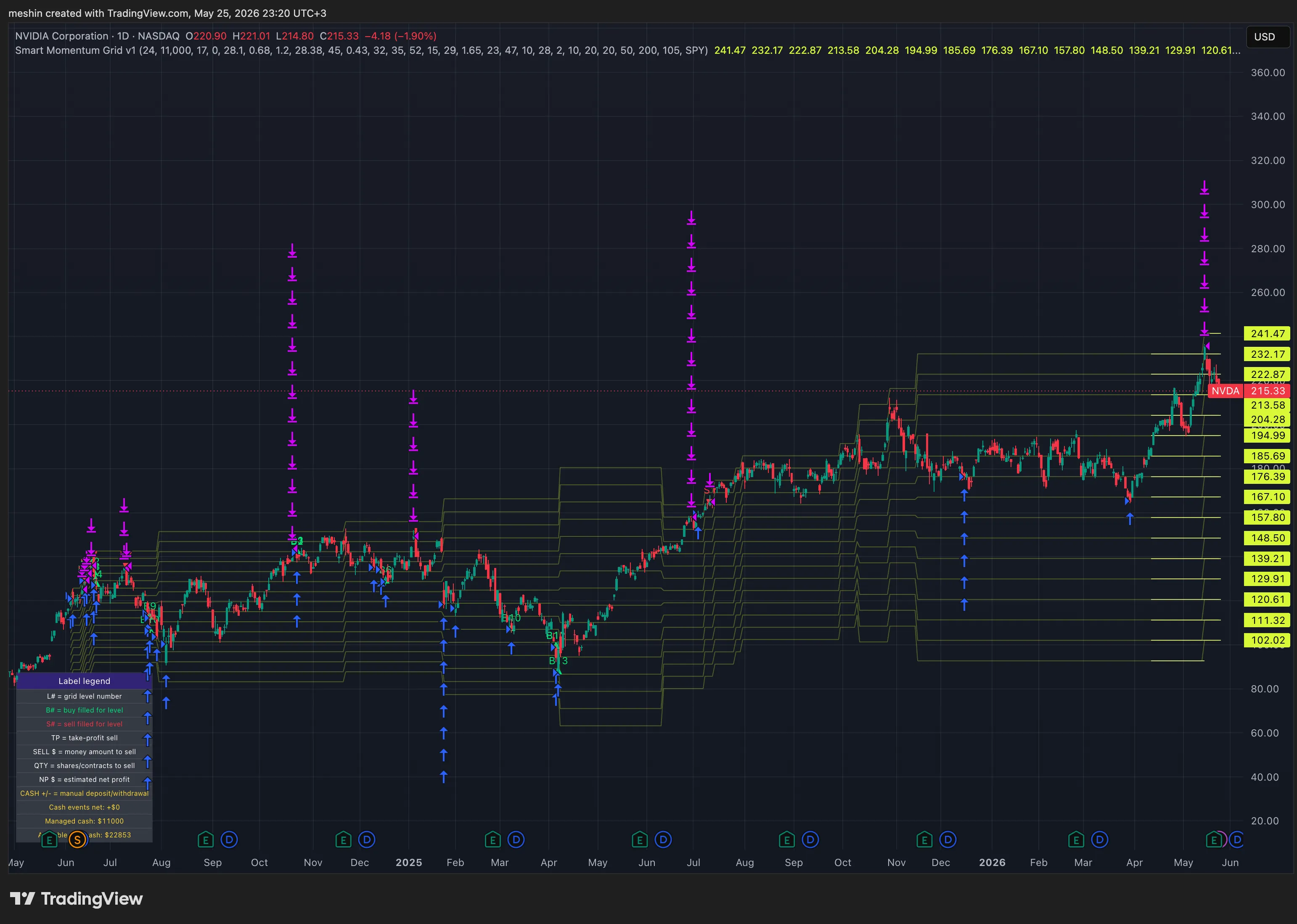

NASDAQ

NASDAQNVDA

NVIDIA Corporation

Net profit (historical)

+143.40%

Buy & hold

+84.10%

1.71x vs buy & hold (historical) View backtest -

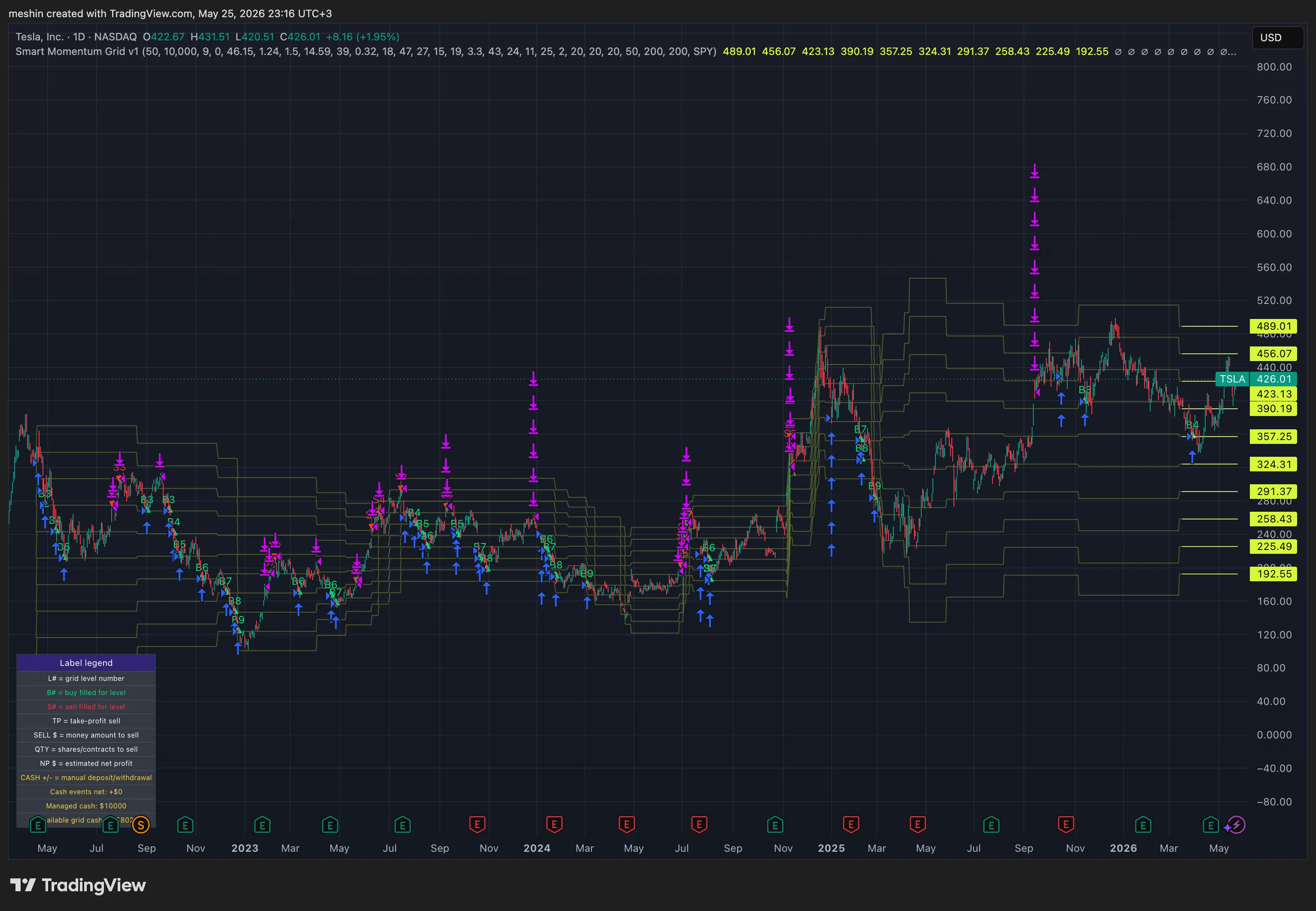

NASDAQ

NASDAQTSLA

Tesla, Inc.

Net profit (historical)

+174.53%

Buy & hold

+100.81%

1.73x vs buy & hold (historical) View backtest -

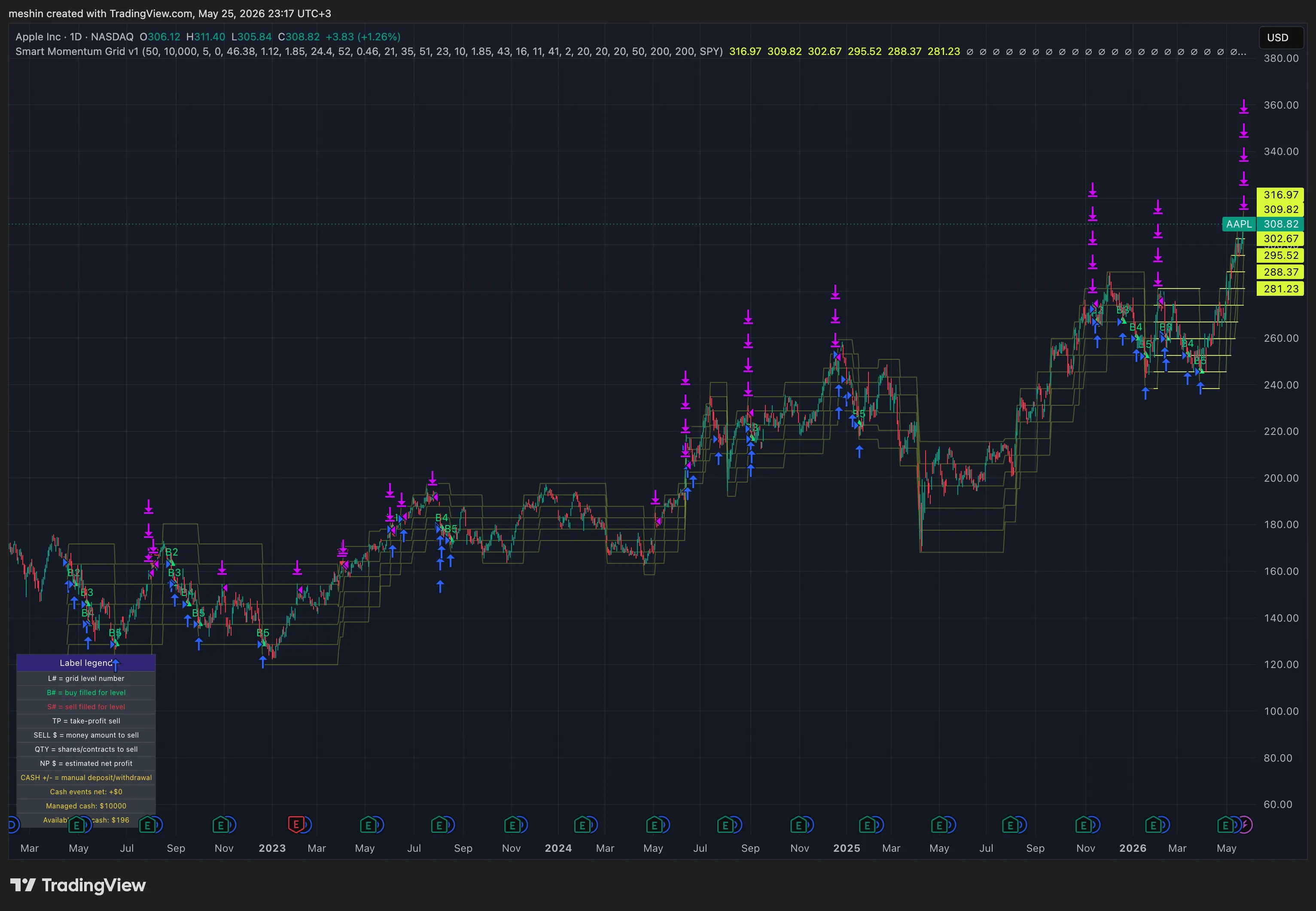

NASDAQ

NASDAQAAPL

Apple Inc.

Net profit (historical)

+133.34%

Buy & hold

+110.84%

1.20x vs buy & hold (historical) View backtest -

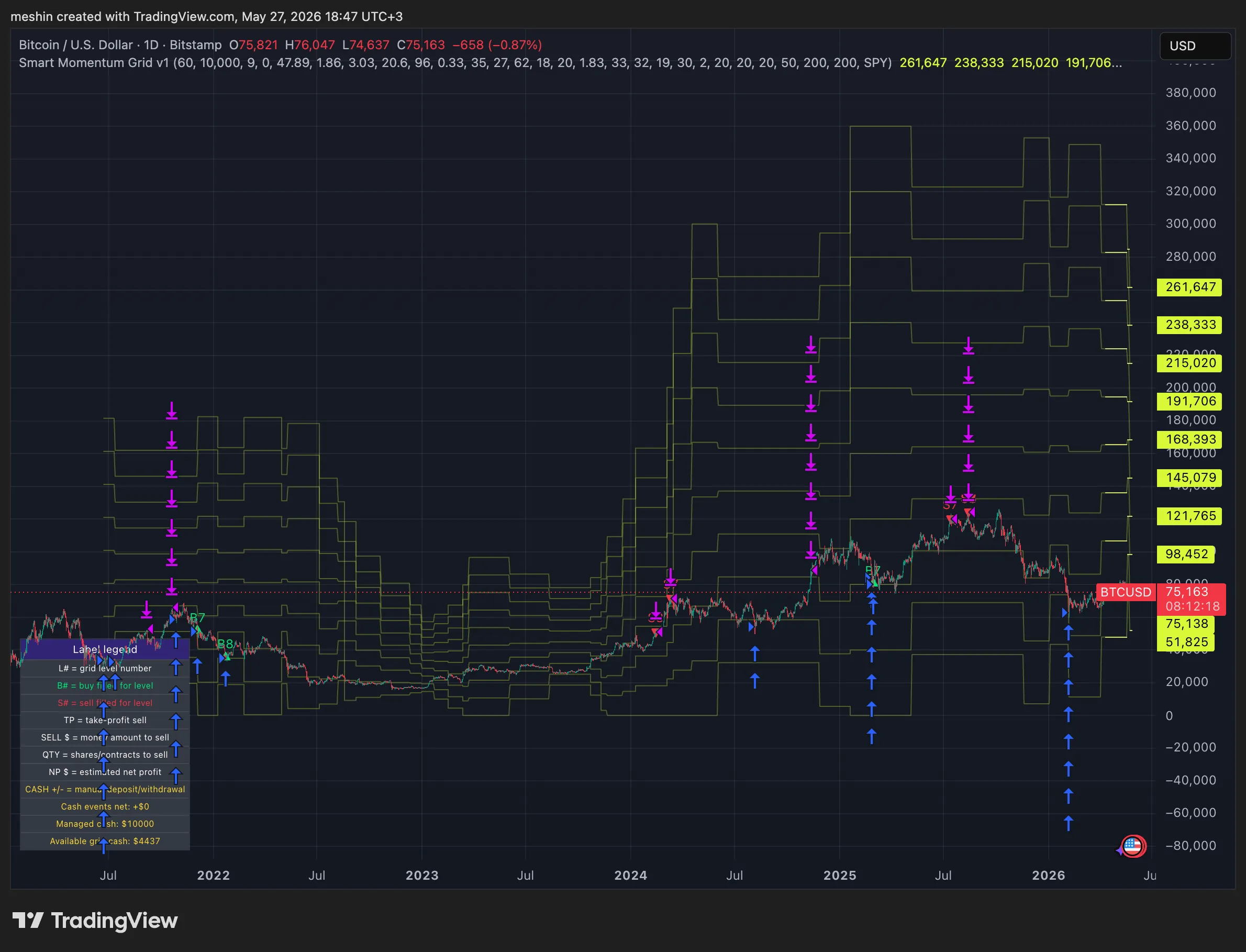

Bitstamp

BitstampBTC

Bitcoin

Net profit (historical)

+302.24%

Buy & hold

+129.68%

2.33x vs buy & hold (historical) View backtest

How a backtest run is recorded

Each example here is an optimization run over a strategy like the skeleton below. TradingTune sweeps the numeric inputs, records every cycle, and stores a one-line run summary you can export and re-import.

A strategy worth optimizing (illustrative Pine v5)

Pine v5An illustrative momentum skeleton, not the proprietary Smart Momentum Grid. The int inputs are exactly the values TradingTune sweeps, and commission plus slippage are set so the backtest reflects real trading costs.

//@version=5

strategy("Example Momentum", overlay=true,

commission_type=strategy.commission.percent, commission_value=0.05,

slippage=2, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fastLen = input.int(20, "Fast MA Length", minval=1)

slowLen = input.int(100, "Slow MA Length", minval=1)

rsiLen = input.int(14, "RSI Length", minval=1)

fast = ta.sma(close, fastLen)

slow = ta.sma(close, slowLen)

rsi = ta.rsi(close, rsiLen)

if ta.crossover(fast, slow) and rsi > 50

strategy.entry("Long", strategy.long)

if ta.crossunder(fast, slow)

strategy.close("Long")What one run's summary records (metadata.csv)

CSVAlongside the per-cycle results, each run stores a one-line summary: the method used, the cycle counts, and the best cycle found. It re-imports for side-by-side comparison.

runId,optMethod,startedAt,totalCycles,cyclesCompleted,bestCycle,bestNetProfitPct

2026-05-20T14:02:11.880Z,bisection_then_tpe,2026-05-20T14:02:11.880Z,240,240,137,318.6Read this first

Optimization is a multiplier, not a magic pill.

The example above is illustrative, not a promise: optimization is not a button that prints money. TradingTune helps tune a strategy you already believe in; it cannot invent an edge that was never there. Two things have to be true, in this order, before any optimization is worth running.

Good strategy × right parameters = results

Miss either factor and you are multiplying by zero.

- 1

A strategy with a real edge

Optimization tunes the dials of a strategy. It cannot create signal from noise. If the underlying idea has no edge, no combination of settings will save it: you will only find the parameters that fit the past best and then fall apart live. Garbage in, garbage out. Start with a strategy you understand and believe in.

- 2

The right parameters

Even a genuinely good strategy, run on the wrong inputs, leaves most of its edge on the table, and at worst looks broken when it is not. The default settings are almost never optimal for your market and timeframe. This is the half TradingTune automates: it sweeps the parameter space and surfaces the settings that actually perform.

Bring the edge, you tune the settings. Skip the first half and you are polishing a strategy that was never going to work. Skip the second and you are trading a good idea with the brakes on. The examples above illustrate the second half, on the founder's own strategy.

Run it on your own symbols

Install TradingTune and optimize any TradingView strategy on any market, right in your browser. Free tier, no API keys. A free account is required to run.

Add to Chrome, it's free